Tutorial 06 - Cross-sectional rotation and portfolio construction

Executed tutorial notebook. This page is generated from

examples/notebooks/quant_trading/06_cross_sectional_rotation_portfolio.ipynb and includes markdown cells, code cells, stdout, tables, and captured figures from the committed notebook.

Tutorial Navigation

| Track | Tutorial notebook |

|---|---|

| Roadmap | Tutorial 00 - Roadmap |

| Strategy Lab | 01 Trend-Following Lab |

| Tutorial Sequence | 01 Real Market Data and Feature Factory |

| Tutorial Sequence | 02 Decomposition-aware MA and MACD |

| Strategy Lab | 02 Oscillation-Reversion Lab |

| Strategy Expansion | 03 Method-Specific Variants |

| Tutorial Sequence | 03 Residual Mean Reversion |

| Strategy Expansion | 04 Component Pair Trading |

| Tutorial Sequence | 04 Donchian Breakout |

| Tutorial Sequence | 05 Pair-Spread Stat-Arb |

| Tutorial Sequence | 06 Cross-Sectional Rotation |

| Native SSA Replay | 07 Native SSA High-Return / Low-Drawdown |

Executed Notebook

This notebook turns DeTime features into a portfolio ranking language: trend decides direction, cycle adjusts timing, residual controls overextension and volume/reconstruction features control reliability.

In [1]

import matplotlib.pyplot as plt

import pandas as pd

from quant_trading.data import load_bundled_real_ohlcv_panel, ohlcv_audit_report

from quant_trading.features import walkforward_decompose_ohlcv

from quant_trading.decomposition_features import feature_coverage_report, build_feature_table

from quant_trading.strategy_baselines import buy_and_hold_weights

from quant_trading.strategy_rotation import (

classic_momentum_rotation_weights, detime_cross_sectional_score,

detime_long_short_rotation_weights, detime_rotation_weights,

rotation_diagnostic_table, volume_availability,

)

from quant_trading.validation import compare_weight_strategies, turnover_report

1. Load real offline market data

In [2]

tickers = ["AUDUSD=X", "NZDUSD=X", "EURUSD=X", "GBPUSD=X"]

ohlcv = load_bundled_real_ohlcv_panel(tickers, min_observations=120)

ohlcv = {field: table.tail(760).copy() for field, table in ohlcv.items()}

prices = ohlcv["Close"]

volumes = ohlcv.get("Volume")

print("volume_available:", volume_availability(volumes))

ohlcv_audit_report(ohlcv)

stdout

volume_available: False

text/html

| ticker | first_timestamp | last_timestamp | observations | close_missing_ratio | volume_missing_ratio | zero_volume_ratio | min_close | max_close | median_volume | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | AUDUSD=X | 2015-02-02 | 2018-01-02 | 760 | 0.0 | 0.0 | 1.0 | 0.686106 | 0.811293 | 0.0 |

| 1 | NZDUSD=X | 2015-02-02 | 2018-01-02 | 760 | 0.0 | 0.0 | 1.0 | 0.626684 | 0.772380 | 0.0 |

| 2 | EURUSD=X | 2015-02-02 | 2018-01-02 | 760 | 0.0 | 0.0 | 1.0 | 1.039047 | 1.202906 | 0.0 |

| 3 | GBPUSD=X | 2015-02-02 | 2018-01-02 | 760 | 0.0 | 0.0 | 1.0 | 1.203935 | 1.588512 | 0.0 |

2. Build walk-forward asset features

In [3]

features = walkforward_decompose_ohlcv(

ohlcv,

method="STL",

period="auto",

period_candidates=(63, 126, 252),

train_window=504,

step=5,

z_window=63,

)

feature_coverage_report(features).query("feature in ['trend_slope', 'trend_strength', 'cycle_slope', 'residual_z', 'residual_abs_z', 'volume_participation']").head(18)

text/html

| feature | asset | observations | non_null | coverage | first_valid | last_valid | |

|---|---|---|---|---|---|---|---|

| 12 | trend_slope | AUDUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 13 | trend_slope | NZDUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 14 | trend_slope | EURUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 15 | trend_slope | GBPUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 20 | trend_strength | AUDUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 21 | trend_strength | NZDUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 22 | trend_strength | EURUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 23 | trend_strength | GBPUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 32 | cycle_slope | AUDUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 33 | cycle_slope | NZDUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 34 | cycle_slope | EURUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 35 | cycle_slope | GBPUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 48 | residual_z | AUDUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 49 | residual_z | NZDUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 50 | residual_z | EURUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 51 | residual_z | GBPUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 52 | residual_abs_z | AUDUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

| 53 | residual_abs_z | NZDUSD=X | 760 | 257 | 0.338158 | 2017-01-05 | 2018-01-02 |

In [4]

build_feature_table(prices, features).tail(3).iloc[:, :12].round(4)

text/html

| component_stability | cycle | cycle_amplitude | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AUDUSD=X | EURUSD=X | GBPUSD=X | NZDUSD=X | AUDUSD=X | EURUSD=X | GBPUSD=X | NZDUSD=X | AUDUSD=X | EURUSD=X | GBPUSD=X | NZDUSD=X | |

| Date | ||||||||||||

| 2017-12-29 | 0.9957 | 0.9939 | 0.9935 | 0.9935 | -0.0227 | -0.0174 | 0.0056 | -0.0092 | 0.0306 | 0.0198 | 0.0103 | 0.0311 |

| 2018-01-01 | 0.9959 | 0.9943 | 0.9932 | 0.9941 | -0.0147 | -0.0086 | 0.0114 | 0.0075 | 0.0306 | 0.0187 | 0.0100 | 0.0304 |

| 2018-01-02 | 0.9959 | 0.9943 | 0.9932 | 0.9941 | -0.0147 | -0.0086 | 0.0114 | 0.0075 | 0.0306 | 0.0187 | 0.0100 | 0.0304 |

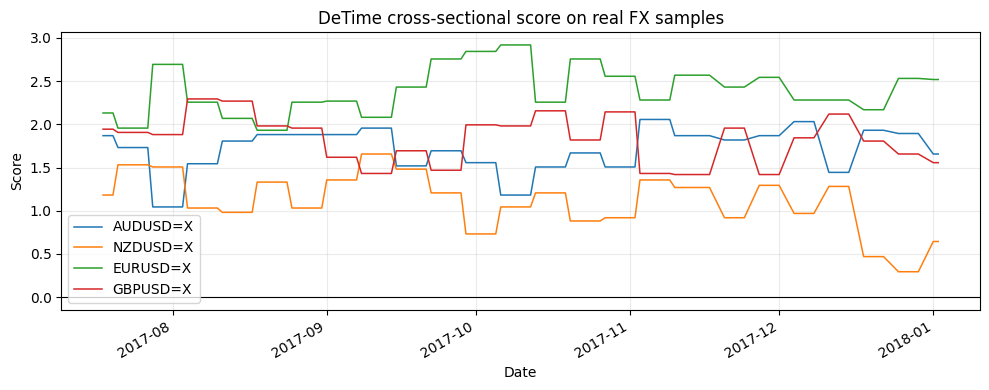

3. Inspect the DeTime rotation score

In [5]

score = detime_cross_sectional_score(prices, features)

score.tail(5).round(3)

text/html

| AUDUSD=X | NZDUSD=X | EURUSD=X | GBPUSD=X | |

|---|---|---|---|---|

| Date | ||||

| 2017-12-27 | 1.894 | 0.294 | 2.531 | 1.656 |

| 2017-12-28 | 1.894 | 0.294 | 2.531 | 1.656 |

| 2017-12-29 | 1.894 | 0.294 | 2.531 | 1.656 |

| 2018-01-01 | 1.656 | 0.644 | 2.519 | 1.556 |

| 2018-01-02 | 1.656 | 0.644 | 2.519 | 1.556 |

In [6]

fig, ax = plt.subplots(figsize=(10, 4))

score.tail(120).plot(ax=ax, linewidth=1.1)

ax.axhline(0, color="black", linewidth=0.8)

ax.set_title("DeTime cross-sectional score on real FX samples")

ax.set_ylabel("Score")

ax.grid(True, alpha=0.25)

plt.tight_layout()

plt.show()

image/png

In [7]

rotation_diagnostic_table(prices, features, tail=2).round(4)

text/html

| date | asset | score | trend_strength | cycle_slope | residual_z | volume_participation | |

|---|---|---|---|---|---|---|---|

| 0 | 2018-01-01 | EURUSD=X | 2.5188 | 0.1228 | 0.0016 | -0.4600 | 1.25 |

| 1 | 2018-01-01 | AUDUSD=X | 1.6563 | 0.0496 | 0.0010 | 0.2019 | 1.25 |

| 2 | 2018-01-01 | GBPUSD=X | 1.5562 | 0.0393 | 0.0011 | 0.1007 | 1.25 |

| 3 | 2018-01-01 | NZDUSD=X | 0.6438 | -0.0190 | 0.0036 | -0.8123 | 1.25 |

| 4 | 2018-01-02 | EURUSD=X | 2.5188 | 0.1228 | 0.0016 | -0.4600 | 1.25 |

| 5 | 2018-01-02 | AUDUSD=X | 1.6563 | 0.0496 | 0.0010 | 0.2019 | 1.25 |

| 6 | 2018-01-02 | GBPUSD=X | 1.5562 | 0.0393 | 0.0011 | 0.1007 | 1.25 |

| 7 | 2018-01-02 | NZDUSD=X | 0.6438 | -0.0190 | 0.0036 | -0.8123 | 1.25 |

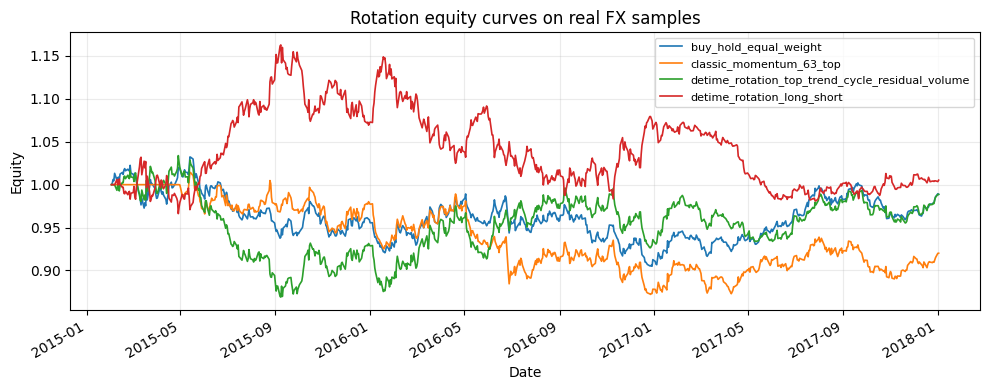

4. Backtest a compact rotation suite

In [8]

strategies = {

"buy_hold_equal_weight": buy_and_hold_weights(prices),

"classic_momentum_63_top": classic_momentum_rotation_weights(prices, lookback=63, top_n=2, rebalance_freq="W-FRI", vol_target=None),

"detime_rotation_top_trend_cycle_residual_volume": detime_rotation_weights(prices, features, top_n=2, rebalance_freq="W-FRI", vol_target=None),

"detime_rotation_long_short": detime_long_short_rotation_weights(prices, features, top_n=2, bottom_n=2),

}

comparison, results = compare_weight_strategies(prices, strategies, fee_bps=1.0, slippage_bps=2.0)

comparison[["total_return", "sharpe", "max_drawdown", "average_turnover"]].round(4)

text/html

| total_return | sharpe | max_drawdown | average_turnover | |

|---|---|---|---|---|

| strategy | ||||

| detime_rotation_long_short | 0.0052 | 0.0686 | -0.1563 | 0.0572 |

| detime_rotation_top_trend_cycle_residual_volume | -0.0112 | 0.0095 | -0.1596 | 0.0289 |

| buy_hold_equal_weight | -0.0115 | -0.0085 | -0.1234 | 0.0000 |

| classic_momentum_63_top | -0.0799 | -0.2850 | -0.1403 | 0.0461 |

In [9]

fig, ax = plt.subplots(figsize=(10, 4))

for name, result in results.items():

result.equity.plot(ax=ax, linewidth=1.2, label=name)

ax.set_title("Rotation equity curves on real FX samples")

ax.set_ylabel("Equity")

ax.legend(loc="best", fontsize=8)

ax.grid(True, alpha=0.25)

plt.tight_layout()

plt.show()

image/png

In [10]

turnover_report(strategies).round(4)

text/html

| average_turnover | median_turnover | max_turnover | average_gross_exposure | |

|---|---|---|---|---|

| strategy | ||||

| buy_hold_equal_weight | 0.0000 | 0.0000 | 0.0 | 1.0000 |

| classic_momentum_63_top | 0.0461 | 0.0000 | 2.0 | 0.9158 |

| detime_rotation_top_trend_cycle_residual_volume | 0.0289 | 0.0000 | 2.0 | 0.9947 |

| detime_rotation_long_short | 0.0572 | 0.0034 | 3.0 | 1.2333 |

5. Live-data extension

Run run_column_06_cross_sectional_rotation.py without --use-bundled-sample to use sector ETFs and real equity/ETF volume. In the bundled FX sample, raw volume is unavailable, so volume is neutral rather than invented.