Tutorial 05 - Pair spread decomposition and stat-arb

Executed tutorial notebook. This page is generated from

examples/notebooks/quant_trading/05_pairs_spread_decomposition_stat_arb.ipynb and includes markdown cells, code cells, stdout, tables, and captured figures from the committed notebook.

Tutorial Navigation

| Track | Tutorial notebook |

|---|---|

| Roadmap | Tutorial 00 - Roadmap |

| Strategy Lab | 01 Trend-Following Lab |

| Tutorial Sequence | 01 Real Market Data and Feature Factory |

| Tutorial Sequence | 02 Decomposition-aware MA and MACD |

| Strategy Lab | 02 Oscillation-Reversion Lab |

| Strategy Expansion | 03 Method-Specific Variants |

| Tutorial Sequence | 03 Residual Mean Reversion |

| Strategy Expansion | 04 Component Pair Trading |

| Tutorial Sequence | 04 Donchian Breakout |

| Tutorial Sequence | 05 Pair-Spread Stat-Arb |

| Tutorial Sequence | 06 Cross-Sectional Rotation |

| Native SSA Replay | 07 Native SSA High-Return / Low-Drawdown |

Executed Notebook

This notebook rewrites pairs trading around spread structure: rolling hedge ratio, spread trend drift, cycle timing and residual deviation.

In [1]

import matplotlib.pyplot as plt

import pandas as pd

from quant_trading.data import load_bundled_real_ohlcv_panel, ohlcv_audit_report

from quant_trading.strategy_pairs import (

walkforward_pair_spread_features, pair_diagnostics, pair_feature_snapshot,

make_classic_pair_weight_grid, make_detime_pair_weight_grid,

compare_pair_suites, run_classical_pair_baselines, run_detime_pair_baselines,

)

from quant_trading.validation import turnover_report, compare_weight_strategies

1. Load real offline market data

In [2]

tickers = ["AUDUSD=X", "NZDUSD=X", "EURUSD=X", "GBPUSD=X"]

pairs = [("AUDUSD=X", "NZDUSD=X"), ("EURUSD=X", "GBPUSD=X")]

ohlcv = load_bundled_real_ohlcv_panel(tickers, min_observations=120)

ohlcv = {field: table.tail(760).copy() for field, table in ohlcv.items()}

prices = ohlcv["Close"]

ohlcv_audit_report(ohlcv)

text/html

| ticker | first_timestamp | last_timestamp | observations | close_missing_ratio | volume_missing_ratio | zero_volume_ratio | min_close | max_close | median_volume | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | AUDUSD=X | 2015-02-02 | 2018-01-02 | 760 | 0.0 | 0.0 | 1.0 | 0.686106 | 0.811293 | 0.0 |

| 1 | NZDUSD=X | 2015-02-02 | 2018-01-02 | 760 | 0.0 | 0.0 | 1.0 | 0.626684 | 0.772380 | 0.0 |

| 2 | EURUSD=X | 2015-02-02 | 2018-01-02 | 760 | 0.0 | 0.0 | 1.0 | 1.039047 | 1.202906 | 0.0 |

| 3 | GBPUSD=X | 2015-02-02 | 2018-01-02 | 760 | 0.0 | 0.0 | 1.0 | 1.203935 | 1.588512 | 0.0 |

2. Build walk-forward spread decomposition features

In [3]

spread_features, spread_panel, beta_panel, pair_specs = walkforward_pair_spread_features(

prices,

pairs,

hedge_window=126,

method="STL",

period=126,

train_window=504,

step=5,

z_window=63,

)

spread_panel.tail()

text/html

| AUDUSD=X__NZDUSD=X | EURUSD=X__GBPUSD=X | |

|---|---|---|

| Date | ||

| 2017-12-27 | -0.078105 | 0.055287 |

| 2017-12-28 | -0.073091 | 0.057506 |

| 2017-12-29 | -0.072003 | 0.060825 |

| 2018-01-01 | -0.072259 | 0.062524 |

| 2018-01-02 | -0.071041 | 0.063328 |

In [4]

pair_diagnostics(prices, pair_specs, hedge_window=90)

text/html

| pair | date | spread | beta | pair_corr_120 | spread_trend_slope | spread_cycle_slope | spread_residual_z | spread_residual_abs_z | volume_liquidity_ok | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | AUDUSD=X/NZDUSD=X | 2018-01-02 | -0.092184 | 0.453700 | 0.632244 | -0.000494 | 0.002530 | -0.386195 | 0.386195 | True |

| 1 | EURUSD=X/GBPUSD=X | 2018-01-02 | 0.076336 | 0.355382 | 0.446730 | 0.000147 | 0.002752 | 1.196764 | 1.196764 | True |

In [5]

snapshot = pair_feature_snapshot(spread_features, tail=2)

snapshot.query("feature in ['trend_slope', 'cycle_slope', 'residual_z', 'residual_abs_z']").tail(16)

text/html

| date | pair | feature | value | |

|---|---|---|---|---|

| 8 | 2018-01-01 | AUDUSD=X__NZDUSD=X | cycle_slope | -0.000361 |

| 9 | 2018-01-01 | EURUSD=X__GBPUSD=X | cycle_slope | 0.000803 |

| 10 | 2018-01-02 | AUDUSD=X__NZDUSD=X | cycle_slope | -0.000361 |

| 11 | 2018-01-02 | EURUSD=X__GBPUSD=X | cycle_slope | 0.000803 |

| 12 | 2018-01-01 | AUDUSD=X__NZDUSD=X | residual_abs_z | 2.174176 |

| 13 | 2018-01-01 | EURUSD=X__GBPUSD=X | residual_abs_z | 0.840480 |

| 14 | 2018-01-02 | AUDUSD=X__NZDUSD=X | residual_abs_z | 2.174176 |

| 15 | 2018-01-02 | EURUSD=X__GBPUSD=X | residual_abs_z | 0.840480 |

| 16 | 2018-01-01 | AUDUSD=X__NZDUSD=X | residual_z | 2.174176 |

| 17 | 2018-01-01 | EURUSD=X__GBPUSD=X | residual_z | -0.840480 |

| 18 | 2018-01-02 | AUDUSD=X__NZDUSD=X | residual_z | 2.174176 |

| 19 | 2018-01-02 | EURUSD=X__GBPUSD=X | residual_z | -0.840480 |

| 64 | 2018-01-01 | AUDUSD=X__NZDUSD=X | trend_slope | -0.000070 |

| 65 | 2018-01-01 | EURUSD=X__GBPUSD=X | trend_slope | 0.000351 |

| 66 | 2018-01-02 | AUDUSD=X__NZDUSD=X | trend_slope | -0.000070 |

| 67 | 2018-01-02 | EURUSD=X__GBPUSD=X | trend_slope | 0.000351 |

3. Backtest classical baselines and DeTime rewrites

In [6]

classic_weights = make_classic_pair_weight_grid(prices, pairs=pairs, lookback=90)

detime_weights = make_detime_pair_weight_grid(prices, pair_specs, spread_features, spread_panel=spread_panel, beta_panel=beta_panel)

all_weights = {**classic_weights, **detime_weights}

comparison, results = compare_weight_strategies(prices, all_weights, fee_bps=1.0, slippage_bps=2.0)

comparison.insert(0, "strategy_group", ["detime_pair" if str(idx).startswith("detime") else "classical_pair" for idx in comparison.index])

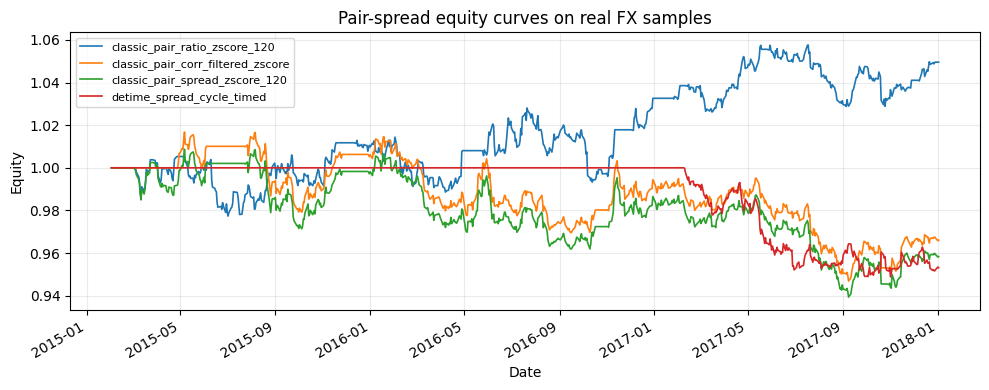

comparison[["strategy_group", "cagr", "sharpe", "max_drawdown", "average_turnover"]].round(4)

text/html

| strategy_group | cagr | sharpe | max_drawdown | average_turnover | |

|---|---|---|---|---|---|

| strategy | |||||

| classic_pair_ratio_zscore_120 | classical_pair | 0.0162 | 0.4520 | -0.0338 | 0.0671 |

| classic_pair_corr_filtered_zscore | classical_pair | -0.0114 | -0.3120 | -0.0687 | 0.0499 |

| classic_pair_spread_zscore_120 | classical_pair | -0.0140 | -0.3748 | -0.0687 | 0.0540 |

| detime_spread_cycle_timed | detime_pair | -0.0158 | -0.7761 | -0.0511 | 0.0146 |

| detime_spread_trend_drift_blocker | detime_pair | -0.0155 | -0.8349 | -0.0575 | 0.0186 |

| detime_spread_residual_z | detime_pair | -0.0176 | -0.9479 | -0.0575 | 0.0186 |

In [7]

leaders = comparison.sort_values("sharpe", ascending=False).head(4).index

fig, ax = plt.subplots(figsize=(10, 4))

for name in leaders:

results[name].equity.plot(ax=ax, linewidth=1.2, label=name)

ax.set_title("Pair-spread equity curves on real FX samples")

ax.set_ylabel("Equity")

ax.legend(loc="best", fontsize=8)

ax.grid(True, alpha=0.25)

plt.tight_layout()

plt.show()

image/png

In [8]

turnover_report(all_weights).round(4)

text/html

| average_turnover | median_turnover | max_turnover | average_gross_exposure | |

|---|---|---|---|---|

| strategy | ||||

| classic_pair_spread_zscore_120 | 0.0540 | 0.0037 | 2.0 | 0.8632 |

| classic_pair_corr_filtered_zscore | 0.0499 | 0.0035 | 2.0 | 0.8171 |

| classic_pair_ratio_zscore_120 | 0.0671 | 0.0000 | 1.0 | 0.8303 |

| detime_spread_residual_z | 0.0186 | 0.0000 | 2.0 | 0.3118 |

| detime_spread_cycle_timed | 0.0146 | 0.0000 | 2.0 | 0.2987 |

| detime_spread_trend_drift_blocker | 0.0186 | 0.0000 | 2.0 | 0.3250 |

4. Live-data extension

Run run_column_05_pairs_spread_decomposition.py without --use-bundled-sample and pass pairs such as KO:PEP, XOM:CVX, MA:V, or SPY:QQQ.