AI Infrastructure Market Pulse

Executed Notebook

This notebook asks how a defined AI-infrastructure market-price basket moved over the selected window. The basket is a public price proxy for attention around compute, cloud, chips, platforms, and adjacent high-interest names.

The output is a basket definition, a source card, trend-index figures, return-versus-trend comparison, and edge-trimmed residual events. Revenue, capex, margins, and valuation require official financial data.

In [1]

from pathlib import Path

import os

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from examples.hot_trends.data import (

HotTrendDataError,

append_real_snapshot,

build_arxiv_monthly_counts,

fetch_coingecko_market_chart,

fetch_defillama_stablecoin_chains,

fetch_github_repo_metadata,

fetch_github_stargazers,

fetch_huggingface_models,

fetch_wikipedia_pageviews,

source_audit_table,

)

from examples.hot_trends.decomposition import (

component_summary,

decompose_table,

editorial_priority,

residual_event_table,

)

from examples.hot_trends.scoring import article_publication_phrasing

pd.set_option("display.max_columns", 80)

pd.set_option("display.max_rows", 80)

plt.rcParams.update({"axes.grid": True})

CACHE_DIR = Path("examples/hot_trends/cache")

OUTPUT_DIR = Path("examples/hot_trends/outputs")

CACHE_DIR.mkdir(parents=True, exist_ok=True)

OUTPUT_DIR.mkdir(parents=True, exist_ok=True)

def save_table(df, name):

path = OUTPUT_DIR / f"{name}.csv"

df.to_csv(path, index=False)

print(f"saved: {path.as_posix()}")

1. Fetch prices through yfinance

In [2]

try:

import yfinance as yf

except Exception as exc:

raise ImportError("Install yfinance to run this notebook: python -m pip install yfinance") from exc

basket_definition = pd.DataFrame([

{"ticker": "NVDA", "role": "GPU accelerator supplier", "boundary": "large-cap chip proxy, not pure infrastructure revenue"},

{"ticker": "AMD", "role": "GPU/CPU accelerator challenger", "boundary": "mixed client, data-center, and gaming exposure"},

{"ticker": "AVGO", "role": "networking and custom silicon", "boundary": "diversified semiconductor and software exposure"},

{"ticker": "MSFT", "role": "cloud and AI platform", "boundary": "large diversified software/cloud company"},

{"ticker": "GOOGL", "role": "cloud, TPU, and AI platform", "boundary": "advertising remains a major business line"},

{"ticker": "AMZN", "role": "cloud infrastructure", "boundary": "retail and marketplace exposure included"},

{"ticker": "META", "role": "AI compute demand and model deployment", "boundary": "advertising platform, not infrastructure vendor"},

{"ticker": "TSLA", "role": "AI narrative and autonomous systems proxy", "boundary": "auto and energy exposure dominates fundamentals"},

])

tickers = basket_definition["ticker"].tolist()

start_date = "2024-01-01"

raw = yf.download(tickers, start=start_date, progress=False, auto_adjust=True)["Close"]

if raw.empty:

raise HotTrendDataError("yfinance returned no market data")

prices = raw.reset_index().melt(id_vars="Date", var_name="ticker", value_name="price").rename(columns={"Date": "date"})

prices = prices.dropna(subset=["price"])

display(basket_definition)

prices.head(20)

text/html

|

ticker |

role |

boundary |

| 0 |

NVDA |

GPU accelerator supplier |

large-cap chip proxy, not pure infrastructure ... |

| 1 |

AMD |

GPU/CPU accelerator challenger |

mixed client, data-center, and gaming exposure |

| 2 |

AVGO |

networking and custom silicon |

diversified semiconductor and software exposure |

| 3 |

MSFT |

cloud and AI platform |

large diversified software/cloud company |

| 4 |

GOOGL |

cloud, TPU, and AI platform |

advertising remains a major business line |

| 5 |

AMZN |

cloud infrastructure |

retail and marketplace exposure included |

| 6 |

META |

AI compute demand and model deployment |

advertising platform, not infrastructure vendor |

| 7 |

TSLA |

AI narrative and autonomous systems proxy |

auto and energy exposure dominates fundamentals |

text/html

|

date |

ticker |

price |

| 0 |

2024-01-02 |

AMD |

138.580002 |

| 1 |

2024-01-03 |

AMD |

135.320007 |

| 2 |

2024-01-04 |

AMD |

136.009995 |

| 3 |

2024-01-05 |

AMD |

138.580002 |

| 4 |

2024-01-08 |

AMD |

146.179993 |

| 5 |

2024-01-09 |

AMD |

149.259995 |

| 6 |

2024-01-10 |

AMD |

148.539993 |

| 7 |

2024-01-11 |

AMD |

148.020004 |

| 8 |

2024-01-12 |

AMD |

146.559998 |

| 9 |

2024-01-16 |

AMD |

158.740005 |

| 10 |

2024-01-17 |

AMD |

160.169998 |

| 11 |

2024-01-18 |

AMD |

162.669998 |

| 12 |

2024-01-19 |

AMD |

174.229996 |

| 13 |

2024-01-22 |

AMD |

168.179993 |

| 14 |

2024-01-23 |

AMD |

168.419998 |

| 15 |

2024-01-24 |

AMD |

178.289993 |

| 16 |

2024-01-25 |

AMD |

180.330002 |

| 17 |

2024-01-26 |

AMD |

177.250000 |

| 18 |

2024-01-29 |

AMD |

177.830002 |

| 19 |

2024-01-30 |

AMD |

172.059998 |

2. Source card and price audit

In [3]

audit = source_audit_table(prices, value_col="price", entity_col="ticker", time_col="date")

source_card = pd.DataFrame([{

"source": "Yahoo Finance through yfinance",

"endpoint": "yfinance.download",

"access_date": pd.Timestamp.today().date().isoformat(),

"query_params": f"tickers={','.join(tickers)}; start={start_date}; auto_adjust=True; field=Close",

"time_range": f"{pd.to_datetime(prices['date']).min().date()} to {pd.to_datetime(prices['date']).max().date()}",

"cache_path": "not cached; outputs saved to examples/hot_trends/outputs",

"interpretation_scope": "public market-price proxy for a defined basket; not fundamentals, valuation, or investment advice",

}])

display(source_card)

audit

text/html

|

source |

endpoint |

access_date |

query_params |

time_range |

cache_path |

interpretation_scope |

| 0 |

Yahoo Finance through yfinance |

yfinance.download |

2026-05-22 |

tickers=NVDA,AMD,AVGO,MSFT,GOOGL,AMZN,META,TSL... |

2024-01-02 to 2026-05-22 |

not cached; outputs saved to examples/hot_tren... |

public market-price proxy for a defined basket... |

text/html

|

series |

first_timestamp |

last_timestamp |

observations |

missing_ratio |

min_value |

max_value |

| 0 |

AMD |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

600 |

0.0 |

78.209999 |

467.510010 |

| 1 |

AMZN |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

600 |

0.0 |

144.570007 |

274.989990 |

| 2 |

AVGO |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

600 |

0.0 |

102.365158 |

439.790009 |

| 3 |

GOOGL |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

600 |

0.0 |

130.322876 |

402.619995 |

| 4 |

META |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

600 |

0.0 |

341.787811 |

788.148987 |

| 5 |

MSFT |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

600 |

0.0 |

351.105774 |

538.658508 |

| 6 |

NVDA |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

600 |

0.0 |

47.539936 |

235.740005 |

| 7 |

TSLA |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

600 |

0.0 |

142.050003 |

489.880005 |

3. Decompose normalized log prices

In [4]

components = decompose_table(prices, entity_col="ticker", time_col="date", value_col="price", method="MA_BASELINE", period=21, trend_window=63, transform="log")

summary = editorial_priority(component_summary(components, entity_col="ticker", time_col="date"), entity_col="ticker")

summary

text/html

|

ticker |

observations |

first_timestamp |

last_timestamp |

trend_last |

trend_slope_per_step |

cycle_strength_proxy |

residual_std |

max_abs_residual_z |

method |

trend_slope_per_step_rank_pct |

cycle_strength_proxy_rank_pct |

max_abs_residual_z_rank_pct |

editorial_priority_score |

| 2 |

AVGO |

600 |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

3.056002 |

0.002033 |

-0.515611 |

0.492248 |

31.542094 |

MA_BASELINE |

1.000 |

1.000 |

0.500 |

0.77500 |

| 3 |

GOOGL |

600 |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

2.996327 |

0.001351 |

-1.894425 |

0.500717 |

38.908369 |

MA_BASELINE |

0.625 |

0.500 |

1.000 |

0.76875 |

| 6 |

NVDA |

600 |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

2.710889 |

0.001477 |

-0.730896 |

0.425016 |

30.472988 |

MA_BASELINE |

0.750 |

0.875 |

0.375 |

0.60625 |

| 7 |

TSLA |

600 |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

3.037916 |

0.001532 |

-1.559972 |

0.528218 |

30.440903 |

MA_BASELINE |

0.875 |

0.750 |

0.250 |

0.56875 |

| 4 |

META |

600 |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

3.277547 |

0.000695 |

-8.994860 |

0.545159 |

34.034109 |

MA_BASELINE |

0.500 |

0.375 |

0.625 |

0.53125 |

| 1 |

AMZN |

600 |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

2.824287 |

0.000536 |

-12.700004 |

0.479970 |

38.328541 |

MA_BASELINE |

0.250 |

0.250 |

0.750 |

0.47500 |

| 5 |

MSFT |

600 |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

3.058471 |

0.000199 |

-28.797940 |

0.536863 |

38.792840 |

MA_BASELINE |

0.125 |

0.125 |

0.875 |

0.46250 |

| 0 |

AMD |

600 |

2024-01-02 00:00:00 |

2026-05-22 00:00:00 |

2.973933 |

0.000667 |

-1.836756 |

0.521744 |

29.756925 |

MA_BASELINE |

0.375 |

0.625 |

0.125 |

0.31250 |

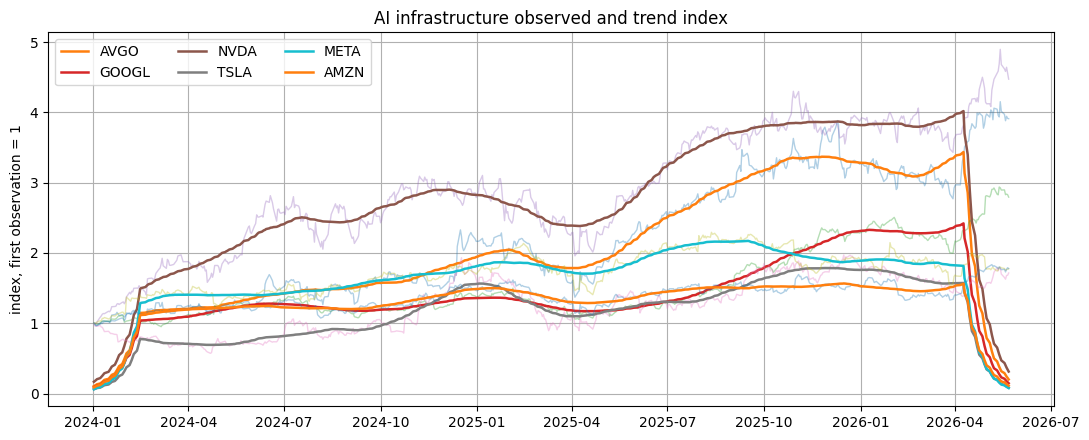

Visualization: AI infrastructure price trend index

The y-axis is an index with each ticker starting at 1. Solid trend lines make basket movement comparable across different share prices. This is a price-proxy view; benchmark and financial-statement evidence are needed before performance or valuation claims.

In [5]

top_tickers = summary["ticker"].head(6).tolist()

fig, ax = plt.subplots(figsize=(11, 4.5))

for ticker in top_tickers:

panel = components.loc[components["ticker"].eq(ticker)].sort_values("date").copy()

panel["date"] = pd.to_datetime(panel["date"])

base = float(panel["observed"].iloc[0])

observed_index = np.exp(panel["observed"] - base)

trend_index = np.exp(panel["trend"] - base)

ax.plot(panel["date"], observed_index, linewidth=1.0, alpha=0.35)

ax.plot(panel["date"], trend_index, linewidth=1.8, label=ticker)

ax.set_title("AI infrastructure observed and trend index")

ax.set_ylabel("index, first observation = 1")

ax.legend(ncol=3, loc="best")

plt.tight_layout()

plt.show()

image/png

4. Cross-sectional AI infrastructure table

In [6]

latest = prices.sort_values("date").groupby("ticker").tail(1).rename(columns={"price": "latest_price"})

first = prices.sort_values("date").groupby("ticker").head(1).rename(columns={"price": "first_price"})[["ticker", "first_price"]]

returns = latest.merge(first, on="ticker", how="left")

returns["total_return_proxy"] = returns["latest_price"] / returns["first_price"] - 1.0

returns.sort_values("total_return_proxy", ascending=False)

text/html

|

date |

ticker |

latest_price |

first_price |

total_return_proxy |

| 6 |

2026-05-22 |

NVDA |

215.330002 |

48.138569 |

3.473128 |

| 3 |

2026-05-22 |

AVGO |

414.140015 |

105.914253 |

2.910144 |

| 5 |

2026-05-22 |

AMD |

467.510010 |

138.580002 |

2.373575 |

| 0 |

2026-05-22 |

GOOGL |

382.970001 |

137.037384 |

1.794639 |

| 4 |

2026-05-22 |

AMZN |

266.320007 |

149.929993 |

0.776296 |

| 2 |

2026-05-22 |

META |

610.260010 |

343.593658 |

0.776110 |

| 7 |

2026-05-22 |

TSLA |

426.010010 |

248.419998 |

0.714878 |

| 1 |

2026-05-22 |

MSFT |

418.570007 |

363.801514 |

0.150545 |

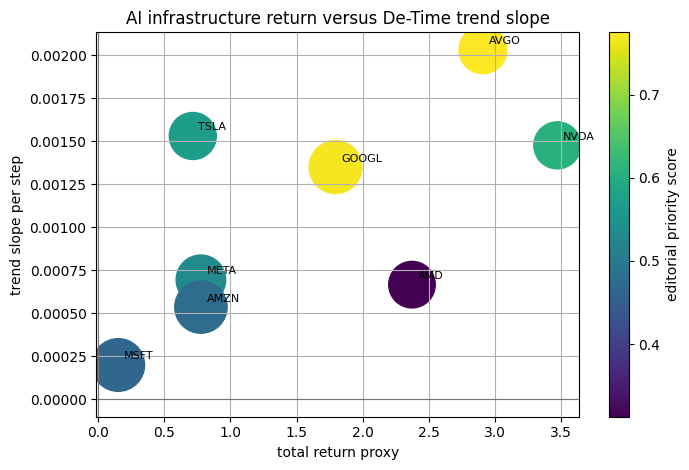

Visualization: return versus trend slope

The x-axis is simple total return over the sampled window. The y-axis is DeTime trend slope; marker size reflects residual shock magnitude. Read the scatter as a basket diagnostic, not as a recommendation.

In [7]

scatter_data = returns.merge(summary[["ticker", "trend_slope_per_step", "max_abs_residual_z", "editorial_priority_score"]], on="ticker", how="left")

fig, ax = plt.subplots(figsize=(7.2, 4.8))

sc = ax.scatter(

scatter_data["total_return_proxy"],

scatter_data["trend_slope_per_step"],

s=80 + scatter_data["max_abs_residual_z"].fillna(0) * 35,

c=scatter_data["editorial_priority_score"],

cmap="viridis",

)

for _, row in scatter_data.iterrows():

ax.annotate(str(row["ticker"]), (row["total_return_proxy"], row["trend_slope_per_step"]), fontsize=8, xytext=(4, 4), textcoords="offset points")

ax.axvline(0, color="0.45", linewidth=0.8)

ax.axhline(0, color="0.45", linewidth=0.8)

ax.set_xlabel("total return proxy")

ax.set_ylabel("trend slope per step")

ax.set_title("AI infrastructure return versus DeTime trend slope")

fig.colorbar(sc, ax=ax, label="editorial priority score")

plt.tight_layout()

plt.show()

image/png

5. Residual events

In [8]

events = residual_event_table(components, entity_col="ticker", time_col="date", top_n=25, trim_edges=63)

events

text/html

|

date |

ticker |

observed |

trend |

season |

residual |

residual_z |

abs_residual_z |

method |

| 0 |

2025-04-04 |

AVGO |

4.977521 |

5.241958 |

0.014480 |

-0.278917 |

-3.450883 |

3.450883 |

MA_BASELINE |

| 1 |

2025-03-10 |

TSLA |

5.403353 |

5.674217 |

0.017037 |

-0.287901 |

-3.276988 |

3.276988 |

MA_BASELINE |

| 2 |

2025-04-08 |

AMD |

4.359398 |

4.608465 |

0.031801 |

-0.280868 |

-3.153715 |

3.153715 |

MA_BASELINE |

| 3 |

2025-10-29 |

AMD |

5.577198 |

5.362060 |

-0.050298 |

0.265437 |

3.070146 |

3.070146 |

MA_BASELINE |

| 4 |

2025-10-27 |

AMD |

5.559412 |

5.352499 |

-0.053735 |

0.260648 |

3.015589 |

3.015589 |

MA_BASELINE |

| 5 |

2025-04-21 |

META |

6.180333 |

6.374351 |

0.038095 |

-0.232114 |

-2.988468 |

2.988468 |

MA_BASELINE |

| 6 |

2025-04-21 |

NVDA |

4.573547 |

4.756973 |

0.037131 |

-0.220557 |

-2.987761 |

2.987761 |

MA_BASELINE |

| 7 |

2025-03-18 |

TSLA |

5.417477 |

5.640343 |

0.039234 |

-0.262100 |

-2.980770 |

2.980770 |

MA_BASELINE |

| 8 |

2024-12-26 |

AVGO |

5.491635 |

5.313243 |

-0.052179 |

0.230571 |

2.932011 |

2.932011 |

MA_BASELINE |

| 9 |

2025-04-07 |

AVGO |

5.029791 |

5.242214 |

0.021533 |

-0.233956 |

-2.887612 |

2.887612 |

MA_BASELINE |

| 10 |

2025-03-11 |

TSLA |

5.440598 |

5.666866 |

0.025627 |

-0.251895 |

-2.863608 |

2.863608 |

MA_BASELINE |

| 11 |

2025-10-28 |

AMD |

5.552998 |

5.357799 |

-0.051031 |

0.246231 |

2.851335 |

2.851335 |

MA_BASELINE |

| 12 |

2025-04-22 |

NVDA |

4.593772 |

4.760719 |

0.043200 |

-0.210147 |

-2.847072 |

2.847072 |

MA_BASELINE |

| 13 |

2025-11-03 |

AMD |

5.559335 |

5.374082 |

-0.059731 |

0.244983 |

2.837123 |

2.837123 |

MA_BASELINE |

| 14 |

2025-04-21 |

TSLA |

5.427150 |

5.630702 |

0.045379 |

-0.248931 |

-2.829580 |

2.829580 |

MA_BASELINE |

| 15 |

2025-04-08 |

AVGO |

5.041978 |

5.243101 |

0.027997 |

-0.229120 |

-2.827026 |

2.827026 |

MA_BASELINE |

| 16 |

2024-12-27 |

AVGO |

5.476813 |

5.317668 |

-0.058443 |

0.217588 |

2.769348 |

2.769348 |

MA_BASELINE |

| 17 |

2024-08-07 |

NVDA |

4.593728 |

4.769571 |

0.025590 |

-0.201433 |

-2.729309 |

2.729309 |

MA_BASELINE |

| 18 |

2025-10-24 |

AMD |

5.533073 |

5.346906 |

-0.049174 |

0.235340 |

2.727268 |

2.727268 |

MA_BASELINE |

| 19 |

2025-04-21 |

AMZN |

5.119908 |

5.262709 |

0.032507 |

-0.175308 |

-2.700299 |

2.700299 |

MA_BASELINE |

| 20 |

2026-01-23 |

AMD |

5.559450 |

5.373623 |

-0.045048 |

0.230875 |

2.676396 |

2.676396 |

MA_BASELINE |

| 21 |

2024-12-24 |

AVGO |

5.468213 |

5.309195 |

-0.050958 |

0.209977 |

2.673997 |

2.673997 |

MA_BASELINE |

| 22 |

2025-05-27 |

TSLA |

5.894100 |

5.719977 |

-0.055374 |

0.229497 |

2.663114 |

2.663114 |

MA_BASELINE |

| 23 |

2025-04-04 |

NVDA |

4.546352 |

4.743817 |

-0.001253 |

-0.196213 |

-2.658758 |

2.658758 |

MA_BASELINE |

| 24 |

2025-04-08 |

NVDA |

4.567233 |

4.742659 |

0.020547 |

-0.195974 |

-2.655528 |

2.655528 |

MA_BASELINE |

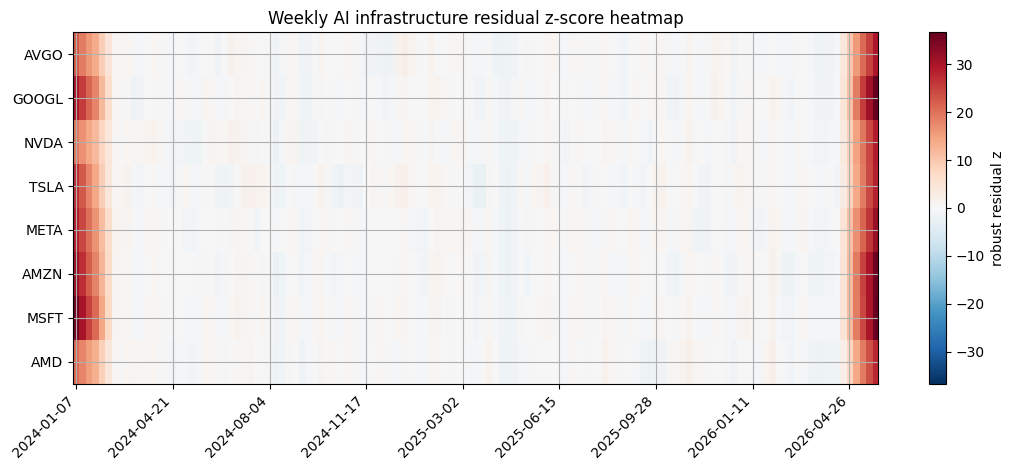

Visualization: AI infrastructure residual heatmap

The heatmap shows weekly residual z-scores by ticker after decomposition. Clusters suggest dates worth matching against launches, earnings, or macro events; edge-trimmed residual tables reduce first/last-window artifacts.

In [9]

residual_grid = components.copy()

residual_grid["residual_z"] = residual_grid.groupby("ticker")["residual"].transform(lambda s: (s - s.median()) / (1.4826 * (s - s.median()).abs().median() + 1e-12))

heat = residual_grid.pivot_table(index="ticker", columns="date", values="residual_z", aggfunc="mean").reindex(summary["ticker"].tolist()).dropna(how="all")

heat = heat.T

heat.index = pd.to_datetime(heat.index)

heat = heat.resample("W").mean().T

values = heat.to_numpy(dtype=float)

absmax = float(np.nanmax(np.abs(values))) if np.isfinite(values).any() else 1.0

fig, ax = plt.subplots(figsize=(11, 4.8))

im = ax.imshow(values, aspect="auto", cmap="RdBu_r", vmin=-absmax, vmax=absmax)

ax.set_yticks(range(len(heat.index)))

ax.set_yticklabels(heat.index)

tick_step = max(1, len(heat.columns) // 8)

xticks = list(range(0, len(heat.columns), tick_step))

ax.set_xticks(xticks)

ax.set_xticklabels([heat.columns[i].strftime("%Y-%m-%d") for i in xticks], rotation=45, ha="right")

ax.set_title("Weekly AI infrastructure residual z-score heatmap")

fig.colorbar(im, ax=ax, label="robust residual z")

plt.tight_layout()

plt.show()

image/png

6. Publication language

In [10]

phrasing = article_publication_phrasing()

phrasing

text/html

|

draft_claim |

evidence_based_phrasing |

| 0 |

This trend predicts the next price move. |

This trend summarizes the observed public seri... |

| 1 |

This model is better because it has more downl... |

Downloads are a public adoption proxy interpre... |

| 2 |

This repo is winning because stars are rising. |

Star velocity measures developer attention for... |

| 3 |

This pageview spike shows the topic matters most. |

Pageviews measure public attention during the ... |

| 4 |

This residual is a buy signal. |

This residual marks an event-like deviation fr... |

In [11]

save_table(source_card, "07_ai_infra_source_card")

save_table(basket_definition, "07_ai_infra_basket_definition")

save_table(audit, "07_ai_infra_market_audit")

save_table(summary, "07_ai_infra_component_summary")

save_table(returns, "07_ai_infra_return_proxy")

save_table(events, "07_ai_infra_residual_events")

save_table(phrasing, "07_ai_infra_publication_phrasing")

stdout

saved: examples/hot_trends/outputs/07_ai_infra_source_card.csv

saved: examples/hot_trends/outputs/07_ai_infra_basket_definition.csv

saved: examples/hot_trends/outputs/07_ai_infra_market_audit.csv

saved: examples/hot_trends/outputs/07_ai_infra_component_summary.csv

saved: examples/hot_trends/outputs/07_ai_infra_return_proxy.csv

saved: examples/hot_trends/outputs/07_ai_infra_residual_events.csv

saved: examples/hot_trends/outputs/07_ai_infra_publication_phrasing.csv