Strategy Lab 01 - Trend-following strategy

Executed tutorial notebook. This page is generated from

examples/notebooks/quant_trading/01_detime_trend_following_strategy_lab.ipynb and includes markdown cells, code cells, stdout, tables, and captured figures from the committed notebook.

Tutorial Navigation

| Track | Tutorial notebook |

|---|---|

| Roadmap | Tutorial 00 - Roadmap |

| Strategy Lab | 01 Trend-Following Lab |

| Tutorial Sequence | 01 Real Market Data and Feature Factory |

| Tutorial Sequence | 02 Decomposition-aware MA and MACD |

| Strategy Lab | 02 Oscillation-Reversion Lab |

| Strategy Expansion | 03 Method-Specific Variants |

| Tutorial Sequence | 03 Residual Mean Reversion |

| Strategy Expansion | 04 Component Pair Trading |

| Tutorial Sequence | 04 Donchian Breakout |

| Tutorial Sequence | 05 Pair-Spread Stat-Arb |

| Tutorial Sequence | 06 Cross-Sectional Rotation |

| Native SSA Replay | 07 Native SSA High-Return / Low-Drawdown |

Executed Notebook

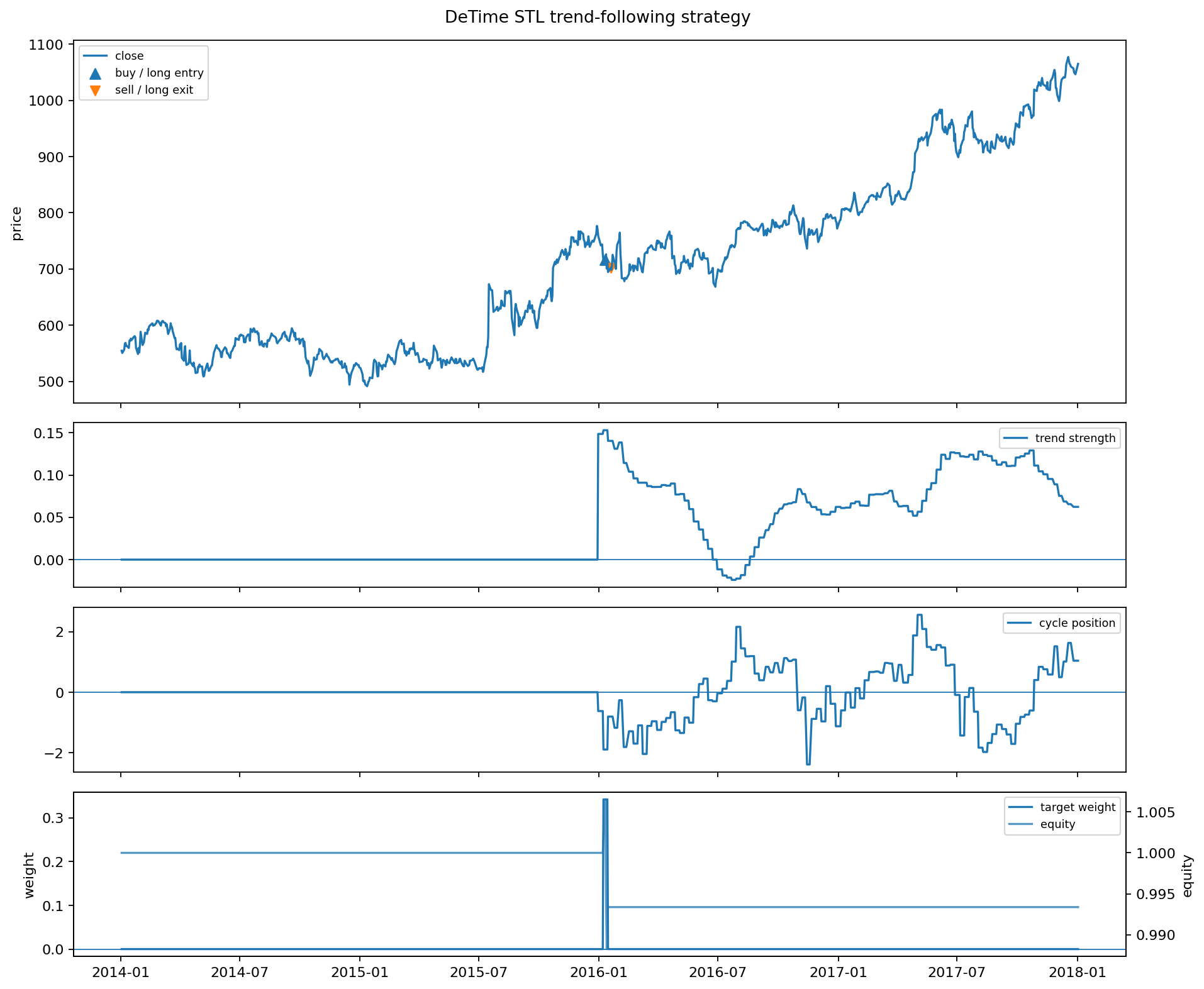

这篇只做一件事:用 DeTime 分解出来的 trend 直接产生交易信号。

策略逻辑:

trend_slope > 0且trend_strength足够强,说明进入上涨趋势状态。cycle_position不在过热区,避免在周期顶部追进去。residual_abs_z不过大,避免追到结构外的异常拉伸。- 如果有成交量分解,则用

volume_trend_slope / volume_residual_z确认参与度。 - 信号在第 t 根 bar 结束后生成,回测用下一根 bar 的开盘价成交。

In [1]

from pathlib import Path

import pandas as pd

from IPython.display import Image, display

from quant_trading.data import load_sample_goog_ohlcv

from quant_trading.decomposition_features import walkforward_price_volume_features

from quant_trading.strategy_lab import (

TrendFollowingConfig,

OscillationReversionConfig,

backtest_signal_set,

execution_price_panel,

decomposition_trend_following_signals,

decomposition_oscillation_reversion_signals,

plot_signal_analysis,

stats_table,

)

from quant_trading.strategy_baselines import (

buy_and_hold_weights,

dual_moving_average_weights,

bollinger_mean_reversion_weights,

)

from quant_trading.strategy_lab import backtest_target_weights_next_bar

CHART_DIR = Path("examples/quant_trading/reports/strategy_lab/charts")

In [2]

ohlcv = load_sample_goog_ohlcv(trim_start="2014-01-01")

symbol = "GOOG"

close = ohlcv["Close"].rename(symbol).to_frame()

volume = ohlcv["Volume"].rename(symbol).to_frame()

execution_prices = execution_price_panel(ohlcv, field="Open", next_bar=True)

execution_prices.columns = [symbol]

features = walkforward_price_volume_features(

close, volume, method="STL", period=126, train_window=504, step=5, z_window=63

)

list(features)[:8]

text/plain

['trend',

'cycle',

'residual',

'trend_slope',

'trend_acceleration',

'trend_strength',

'trend_gap',

'cycle_z']

In [3]

signal = decomposition_trend_following_signals(

close,

features,

config=TrendFollowingConfig(

entry_trend_strength=0.15,

exit_trend_strength=0.02,

max_entry_cycle_position=1.25,

max_entry_residual_abs_z=2.5,

use_volume_confirmation=True,

allow_short=False,

),

name="detime_STL_trend_following",

)

bt = backtest_signal_set(

close, signal, execution_prices=execution_prices, fee_bps=5, slippage_bps=2, periods_per_year=252

)

baselines = {

"buy_hold": buy_and_hold_weights(close),

"classic_sma_20_100": dual_moving_average_weights(close, fast=20, slow=100),

}

results = {signal.name: bt}

for name, weights in baselines.items():

results[name] = backtest_target_weights_next_bar(

close, weights, execution_prices=execution_prices, fee_bps=5, slippage_bps=2, periods_per_year=252, name=name

)

stats_table(results)

text/html

| strategy | total_return | cagr | sharpe | max_drawdown | calmar | volatility | hit_rate | trade_win_rate | average_trade_directional_return | orders | round_trips | median_bars_held | average_turnover | average_gross_exposure | fee_bps | slippage_bps | periods_per_year | execution_model | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | buy_hold | 0.887479 | 0.172116 | 0.799165 | -0.192787 | 0.892778 | 0.232171 | 0.524802 | NaN | NaN | 1.0 | 0.0 | NaN | 0.000000 | 1.000000 | 5.0 | 2.0 | 252.0 | signal_on_bar_t_fill_next_bar_open_or_proxy |

| 2 | classic_sma_20_100 | 0.010232 | 0.002548 | 0.107019 | -0.297157 | 0.008576 | 0.187310 | 0.332341 | 0.25 | -0.002942 | 17.0 | 8.0 | 67.0 | 0.016865 | 0.630952 | 5.0 | 2.0 | 252.0 | signal_on_bar_t_fill_next_bar_open_or_proxy |

| 0 | detime_STL_trend_following | -0.006633 | -0.001663 | -0.213044 | -0.018183 | -0.091433 | 0.007671 | 0.002976 | 0.00 | -0.018574 | 2.0 | 1.0 | 5.0 | 0.000678 | 0.001696 | 5.0 | 2.0 | 252.0 | signal_on_bar_t_fill_next_bar_open_or_proxy |

In [4]

bt.orders.tail(10)

text/html

| asset | signal_date | fill_date | action | previous_weight | new_weight | delta_weight | fill_price | |

|---|---|---|---|---|---|---|---|---|

| 0 | GOOG | 2016-01-08 | 2016-01-11 | buy | 0.000000 | 0.341871 | 0.341871 | 716.609985 |

| 1 | GOOG | 2016-01-15 | 2016-01-19 | sell | 0.341871 | 0.000000 | -0.341871 | 703.299988 |

In [5]

bt.trades.tail(10)

text/html

| asset | side | entry_signal_date | entry_fill_date | exit_signal_date | exit_fill_date | entry_price | exit_price | bars_held | entry_weight | directional_return | approx_weighted_return_after_cost | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | GOOG | long | 2016-01-08 | 2016-01-11 | 2016-01-15 | 2016-01-19 | 716.609985 | 703.299988 | 5 | 0.341871 | -0.018574 | -0.006589 |

In [6]

out = CHART_DIR / "notebook_01_trend_following.png"

plot_signal_analysis(ohlcv, signal, bt, asset=symbol, output_path=out, title="DeTime STL trend-following strategy")

display(Image(filename=str(out)))

out.as_posix()

image/png

text/plain

'examples/quant_trading/reports/strategy_lab/charts/notebook_01_trend_following.png'